Wunder Predicts 2023

WunderPredicts Not your grandmother’s end-of-year trend report. This is WunderPredicts. Mapping the soon-to-trend. Here’s looking at you, 2023.

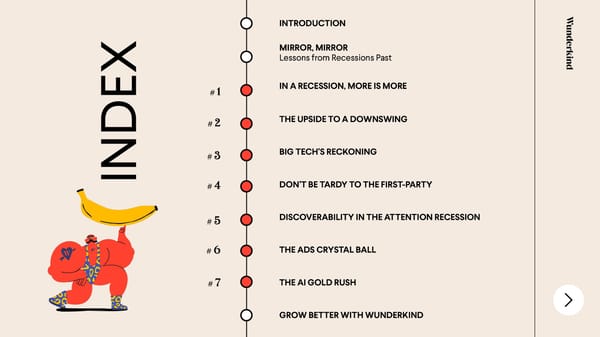

INTRODUCTION MIRROR, MIRROR X Lessons from Recessions Past E #1 IN A RECESSION, MORE IS MORE #2 THE UPSIDE TO A DOWNSWING #3 BIG TECH’S RECKONING IND #4 DON’T BE TARDY TO THE FIRST-PARTY #5 DISCOVERABILITY IN THE ATTENTION RECESSION #6 THE ADS CRYSTAL BALL #7 THE AI GOLD RUSH GROW BETTER WITH WUNDERKIND

Change is a constant -it’s the context within which brands are made, defined, and must grow. This has never been more true than now –a statement made on the heels of constant, unprecedented, and accelerated change -feels less philosophical and more tactical than it has in years past. As we close the book on 2022, we thought it appropriate –even necessary –to make an educated bet on the themes that will define 2023. If one lesson resonates from the last few years, it is that great brands are born at the cusp of big inflection moments.And in what can often feel like a winner-take- intro. all ecosystem, the need to get the foundations right cannot be over-emphasized. Exceptional, era-defying brands have the “The four most dangerous words in following in common – the English langauage -this time it’s • Singular Vision–One north star. They rally different” - Sir John Templeton their entire organization across operations toward a shared goal. In a turbulent environment with many shifting • Agility –With a crystal clear direction in priorities, brands need to keep the above in place, remaining nimble is of the utmost mind, and leverage the data they have on their importance, both in terms of bringing customers to make informed, timely decisions. newness to market, and pivoting messaging This helps them deliver resonant, richer strategically in response to shifts in experiences that forge deeper consumer customer feedback, attitudes, and relationships –in fact, CMOs citeconsumer behaviors. expectations as the #1 driving force behind brand strategy. • Consumer at the Forefont –Finally, bringing With that in mind, let’s dive in on our bets for consumers along with them on the journey 2023. to create a holistic brand universe.

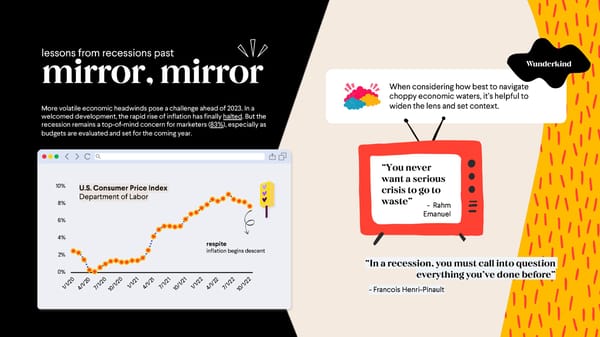

lessons from recessions past mirror, mirror When considering how best to navigate choppy economic waters, it’s helpful to More volatile economic headwinds pose a challenge ahead of 2023. In a widen the lens and set context. welcomed development, the rapid rise of inflation has finally halted. But the recession remains a top-of-mind concern for marketers (83%), especially as budgets are evaluated and set for the coming year. “You never want a serious 10% U.S. Consumer Price Index crisis to go to Department of Labor waste” 8% - Rahm Emanuel 6% 4% respite 2% inflation begins descent “In a recession, you must call into question 0% 0 0 0 0 1 1 1 1 2 2 2 2 everything you’ve done before” 2 2 2 2 2 2 2 2 2 2 2 2 / / 1/ / 1/ 1/ / / 1/ 1 1 /1/ 1/ 1 7/ / 1/1/ 1 1 /1/ 1/ 4/ 7/ 10 4/ 10 4/ 7/ 10 - Francois Henri-Pinault

“It’s only when the tide Feature, Not a Bug Consumer Behavior Reinforced goes out that you realize The SARs Outbreak (2000-04) catapultedChina who has been swimming Since World War II, the US economy has faced naked.” 12recessions (averaging to an occurrence ahead of the rest of the world in digital adoption. every ~6 years), each with its own unique After 2008, consumers lookedto e-commerce as - Warren Buffett characteristics. Most relevant to recall are the a source of discovery, easy comparability, and a 21st century cases –the Dot-Com burst in path to finding deals and discounts. When we 2001 and the Great Recession of 2008. zoom-out, myths about e-commerce were In fact, when President Trump took office in busted through these periods. For example, we 2017, he inherited the single longest, on- once believed instant gratification would be a record, uninterrupted period of economic barrier to online migration. It was believed, for expansion in US history, which came to an end example, that no one would buy clothes without when COVID-19 disrupted the due course of touching and feeling them, and yet, apparel is things. The pandemic in turn, became an now the #1 category purchased online – accelerantfor e-commerceand digitization. consistently. Through the anticipation of challenging times, Conflict Fuels Innovation brands should be aware of structural changes in their environment. Being canny enough to The 2008 recession drovethe rise of the first recognize them and bold enough to invest wave of direct-to-consumer all-stars, including accordingly is what separates changemakers brands like Bonobos and Warby Parker, who from the rest. A silver bullet for success is drove a new era of democratized, digital mythology –your consumer, market, and peer narrative, influence, and a consolidation of set determine your trajectory. growth on platforms like Facebook, Instagram, and YouTube.

WunderPredicts The Six Trends That Will Shape 2023

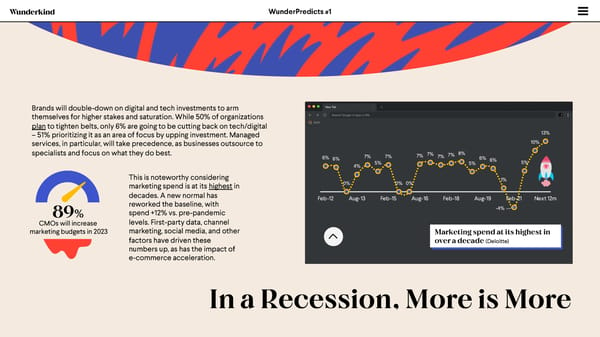

WunderPredicts #1 Brands will double-down on digital and tech investments to arm themselves for higher stakes and saturation. While 50% of organizations planto tighten belts, only 6% are going to be cutting back on tech/digital –51% prioritizing it as an area of focus by upping investment. Managed 13% services, in particular, will take precedence, as businesses outsource to 10% specialists and focus on what they do best. 6% 7% 7% 7% 7% 7% 7% 8% 6% 6% 6% 5% 4% 5% 5% This is noteworthy considering 1% marketing spend is at its highest in 0% 0% 0% decades. A new normal has Feb-12 Aug-13 Feb-15 Aug-16 Feb-18 Aug-19 Feb-21 Next 12m reworked the baseline, with -4% 89% spend +12% vs. pre-pandemic CMOs will increase levels. First-party data, channel marketing budgets in 2023 marketing, social media, and other Marketing spend at its highest in factors have driven these over a decade(Deloitte) numbers up, as has the impact of e-commerce acceleration. In a Recession, More is More

Rec Wu #1 11:11 Notes Done o n Align your budget with m d your strategic goals m e If increasing retention and r relevance, as well as safeguarding k your organization from loss of end market share is deemed important, i then performance and digital n marketing spend is key. d s

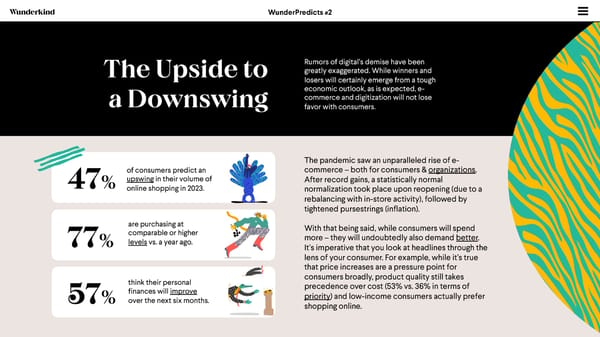

WunderPredicts #2 Rumors of digital’s demise have been The Upside to greatly exaggerated. While winners and losers will certainly emerge from a tough economic outlook, as is expected, e- a Downswing commerce and digitization will not lose favor with consumers. The pandemic saw an unparalleled rise of e- of consumers predict an commerce –both for consumers & organizations. 47% upswingin their volume of After record gains, a statistically normal online shopping in 2023. normalization took place upon reopening (due to a rebalancing with in-store activity), followed by tightened pursestrings (inflation). are purchasing at With that being said, while consumers will spend comparable or higher more –they will undoubtedly also demand better. 77% levelsvs. a year ago. It’s imperative that you look at headlines through the lens of your consumer. For example, while it’s true that price increases are a pressure point for think their personal consumers broadly, product quality still takes finances will improve precedence over cost (53% vs. 36% in terms of 57% over the next six months. priority) and low-income consumers actually prefer shopping online.

11:11 Rec Wu #2 Notes Done Globally, online shopping o n maintains relative stability m d and has normalized. m e Consumers are looking to r prioritize where their hard- earned cash is spent. Make end k sure you capture a portion of i that wallet share. n s d

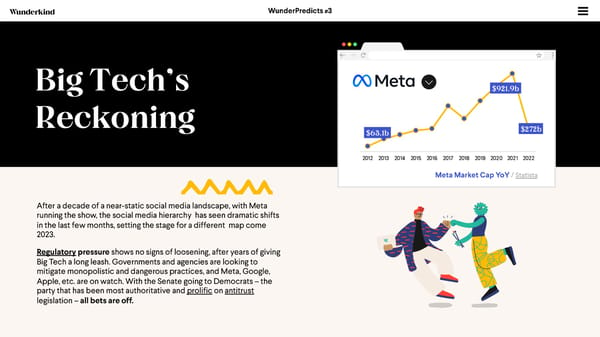

WunderPredicts#3 Big Tech’s $921.9b Reckoning $272b $63.1b 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Meta Market Cap YoY/Statista After a decade of a near-static social media landscape, with Meta running the show, the social media hierarchy has seen dramatic shifts in the last few months, setting the stage for a different map come 2023. Regulatorypressureshows no signs of loosening, after years of giving Big Tech a long leash. Governments and agencies are looking to mitigate monopolistic and dangerous practices, and Meta, Google, Apple, etc. are on watch. With the Senate going to Democrats –the party that has been most authoritative and prolificon antitrust legislation – all bets are off.

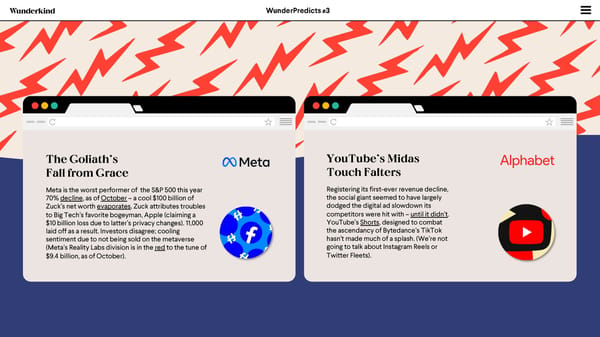

WunderPredicts#3 The Goliath’s YouTube’s Midas Fall from Grace Touch Falters Meta is the worst performer of the S&P 500 this year Registering its first-ever revenue decline, 70% decline, as of October–a cool $100 billion of the social giant seemed to have largely Zuck’s net worth evaporates. Zuck attributes troubles dodged the digital ad slowdown its to Big Tech’s favorite bogeyman, Apple (claiming a competitors were hit with –until it didn’t. $10 billion loss due to latter’s privacy changes). 11,000 YouTube’s Shorts, designed to combat laid off as a result. Investors disagree; cooling the ascendancy of Bytedance’s TikTok sentiment due to not being sold on the metaverse hasn’t made much of a splash. (We’re not (Meta’s Reality Labs division is in the red to the tune of going to talk about Instagram Reels or $9.4 billion, as of October). Twitter Fleets).

WunderPredicts#3 Snap reported its It’s TikTok’s world, Twitter’s Ad exodus lowest quarterly and we are just Musk’s much-delayed sales growth ever living in it acquisition was promptly Video-based platforms In September, TikTok followed by a series of fighting for a piece of the joined the rarified club of disastrous moves too long pie in an increasingly the tech elite, hitting 1 to detail, including firing crowded space. billion users. As nearly almost the entirety of the every other major top brass, and approximate platform races to mimic 80% of total staff. Failed TikTok’s product and be a features and other gaffes recipient of similar followed. success, it was crowned This does not quite make Amazon dropped the topgrossing app in for a stable advertiser draw. out of the trillion 2022 (when combined Rather, unsurprisingly dollar club with its Chinese market leading to an advertiser twin) across iOS and exodus with no end in sight And announced its own Android. It was also the as the platform teeters on spate of 10k job cuts -its most popularapp for both the edge of a potential largest in its operating millennials and Gen Z catastrophe. history. in the US.

11:11 #3 Notes Done Recom Wu Fortune favors the bold –not merely the biggest n Nothing screams change like the giants d shaking in their boots. Brands must take this moment to reevaluate their marketing e budget mix –while search and social ad m spend has its place and importance, it is r increasingly clear that placing all your eggs k in the FAANG basket is risky business and ends brands must focus on shoring up their i owned channels and data warehousing to n truly compete in this new era. d

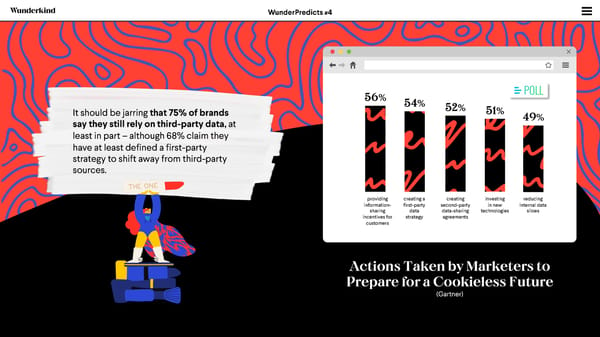

WunderPredicts#4 WunderPredicts #4 8in10 7in10 Americans are troubled 73% expect brand by brand’s usage of their communications tailored personal data. Yet… to their preferences Emailmarketing remainsthe dominant channel by far, even as other channels grow (like text). US Third-Party In light of cookie depreciation and the broader Audience Data $12.3b $13.3b move toward first-party data, marketers are Spending $11.9b predicting a continued rise in the number of $9.7b $11.2b customer data sources, with an average of 18 projectedsources by 2023. However, don’t let this paint an overly rosy picture 2017 2018 2019 2020 2021 –only 14% of brands achieve a true 360 degree view of their customer. Don’t be Tardy to the First-Party

WunderPredicts #4 56% 54% It should be jarring that 75% of brands 52% 51% 49% say they still rely on third-party data, at least in part – although 68% claim they have at least defined a first-party strategy to shift away from third-party sources. providing creating a creating investing reducing information- first-party second-party in new internal data sharing data data-sharing technologies siloes incentives for strategy agreements customers Actions Taken by Marketers to Prepare for a Cookieless Future (Gartner)

11:11 #4 d s Notes Done n d Consumers may claim to be alarmed i n by the usage of their personal data, k e meanwhile they expect and demand a highly personalized and curated r online experience when online e m shopping. Allow customer identity solutions to help fuel personalization d strategies by empowering your marketing teams to recognize n om customers and understand their Wu c wants and needs at every touchpoint. Re

WunderPredicts #5 Not-So-Basic Basics 94% of consumers report Google Cloud’s retail customers registered more website traffic in the first six months of 2022 than receiving irrelevant results all of 2019 combined. E-commerce and owned website e-commerce activity in particular, is red on retailer websites hot. But getting the building blocks right is table stakes, and yet, it’s not a given, not even on brand (something brands are websites. seemingly aware of) 88% Product discovery on your website is not an arena within which you can afford to fumble and this of retailers report pervasive error drives the surge in search abandonment(i.e., when a consumer searches for a search abndonment is a product on a retailer’s website but doesn’t find what they’re looking for), costing retailers more than core issue they contend with, and it costs them $300 billion annuallyin the US alone. customer loyalty of US consumers ditched their online shopping session because they received irrelevant search results on a retailer’s website. More than half say Discoverability 94% they abandon their carts and shop elsewhere if there’s at least one item they can’t find. in the Attention Recession

WunderPredicts #5 $300b 64% High Risk, lost each year from of US retail website High Reward poor online search managers have no clear experiences (US-only) plan for improvement 3 of 4 US consumers shop with brands that personalize interactions and outreach to them and nearly 90% are loyalized 85% to brands that understand their interests. 77% of US consumers avoid websites where they’ve experienced search difficulties of global online and 75% say they are less loyal to a brand when it’s hard to find consumers view a brand what they want on a website. 74% agree that if a company won’t differently after an invest in improving its website, then they don’t want to give unsuccessful search them their money. The numbers are even more dramatic globally –for example, in the UK, 86% of consumers will stop Data | Think with Google frequenting brands with underwhelming search and navigation.

WunderPredicts #5 Keep it Moving YouTube Shorts hit 1.5 billion viewersper month and they TikTok captivated attention spans and wallet share in 2022, view 30 billion Shorts a month. In November, YouTube and with nearly every major social platform copycatting brought Shorts to its TV apps. TikTok’s product, short-form video is showing no indication of slowing down. 140 billion Reels are Signal is the latest app Instagram Reels and YouTube Shortsare major focuses for played daily, per Meta. to debut Stories. their parent companies, as they face economic headwinds and lose share to TikTok. 33% of marketers already invest in Twitter is adding a TikTok rolls out its own short-form video content and one-third of those who don’t TikTok-like discovery marketplace. The plan to do so in 2023. capability. (Note -this average TikTok user is pre-Elon so remains spends an average of For brands looking to incrementality test with short-form to be seen). 24 hoursper month on video content, a potential area that has seen success across the platform. retail formats is user-generated content spotlighted via video, sometimes by white-labeling influencer content.

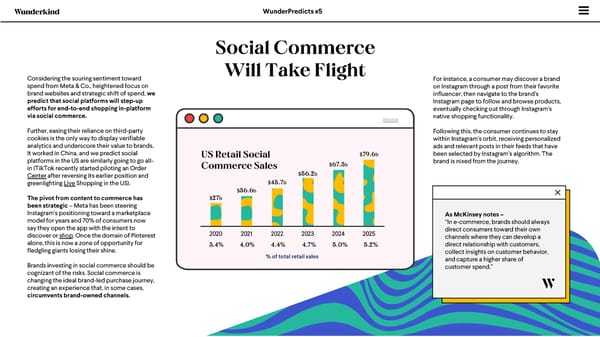

WunderPredicts #5 Social Commerce Considering the souring sentiment toward Will Take Flight For instance, a consumer may discover a brand spend from Meta & Co., heightened focus on on Instagram through a post from their favorite brand websites and strategic shift of spend, we influencer, then navigate to the brand’s predict that social platforms will step-up Instagram page to follow and browse products, efforts for end-to-end shopping in-platform eventually checking out through Instagram’s via social commerce. Source native shopping functionality. Further, easing their reliance on third-party Following this, the consumer continues to stay cookies is the only way to display verifiable within Instagram’s orbit, receiving personalized analytics and underscore their value to brands. ads and relevant posts in their feeds that have It worked in China, and we predict social US Retail Social $79.6b been selected by Instagram’s algorithm. The platforms in the US are similarly going to go all- Commerce Sales $67.3b brand is nixed from the journey. in (TikTok recently started piloting an Order $56.2b Centerafter reversing its earlier position and greenlighting LiveShopping in the US). $45.7b $36.6b The pivot from content to commerce has $27b been strategic –Meta has been steering Instagram’s positioning toward a marketplace As McKinsey notes – model for years and 70% of consumers now “In e-commerce, brands should always say they open the app with the intent to 2020 2021 2022 2023 2024 2025 direct consumers toward their own discover or shop. Once the domain of Pinterest channels where they can develop a alone, this is now a zone of opportunity for 3.4% 4.0% 4.4% 4.7% 5.0% 5.2% direct relationship with customers, fledgling giants losing their shine. collect insights on customer behavior, % of total retail sales and capture a higher share of Brands investing in social commerce should be customer spend.” cognizant of the risks. Social commerce is changing the ideal brand-led purchase journey, creating an experience that, in some cases, circumvents brand-owned channels.

11:11 #5 d s Notes Done n d Brand-led channels should be your i n center of gravity when it comes to k e the primary point of transaction r and revenue. Utilize social e m commerce for discovery and acquisition. Who said you can’t d have your cake and eat it too? n om Wu c Re

WunderPredicts #6 +13% 20 Despite a rocky year for 21 $220b Spend grewby 37% last some, the forecast is rosy year, but slowed in 2022 as –digital ad spending will it normalizedfrom hit $249 billion in the US 20 pandemic growth (similar this year. 23 $249b to e-commerce). Ad dollars are flowing resolutely to digital. In 2019, digital accounted for 56% of total US media ad spend. This year, it will account for 72%. By 2026, digital ad spending will reach$386 billion and make up 81% of total media ad spend. Search Display Within digital, search accounts for 41% of Within display, currently accounting for The Ads total spend, a stronghold in display about half of digital ad spend, growth will predicted to weakenover the next 2 free-fall from 38% to 9% by the end of years, with growth projected to drop by this year as social media platforms lose Crystal Ball more than half in the next year. their shine.

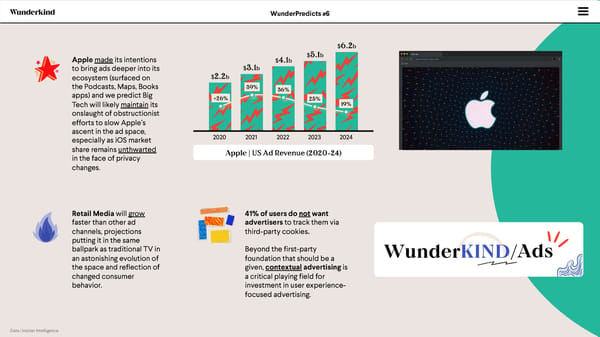

WunderPredicts #6 $6.2b Applemadeits intentions $4.1b $5.1b to bring ads deeper into its $3.1b ecosystem (surfaced on $2.2b the Podcasts, Maps, Books 39% 36% apps) and we predict Big +26% 25% Tech will likely maintain its 19% onslaught of obstructionist efforts to slow Apple’s ascent in the ad space, 2020 2021 2022 2023 2024 especially as iOS market share remains unthwarted Apple | US Ad Revenue (2020-24) in the face of privacy changes. Retail Media will grow 41% of users do notwant faster than other ad advertisers to track them via channels, projections third-party cookies. putting it in the same ballpark as traditional TV in Beyond the first-party WunderKIND/Ads an astonishing evolution of foundation that should be a the space and reflection of given, contextualadvertising is changed consumer a critical playing field for behavior. investment in user experience- focused advertising. Data | Insider Intelligence

11:11 #6 d s Notes Done n d With ad spend booming, make the i n most of your ad strategy by e diversifying how and when you reach k your target audience. For brands who r get in early, retail media solutions e m offer an opportunity to reach a highly-engaged niche of customer. d For advertisers evaluating how best n to target without third-party cookies, om contextual ads allow you to reach c users in relevant environments, at the point in their journey they’re most Wu Re willing to engage.

WunderPredicts #7 WunderPredicts #7 A WORD ON THE TECH HYPE CYCLE “It has echoes of the early days of crypto -genuine excitement about a A new year, a new buzzword–captivating the investorcommunity, holding new, fascinating technology, headlines in its thrall. Marketers are equal parts excited and worried. coupled with outrageous predictions Previous hotly hyped luminaries including crypto, Web3, the Metaverse, etc. are still in the rear window screen. But tech loves a hype cycle. By Fall of of transformative applications that 2022, NFTs were down 90%, the contagion of the cold crypto winter, and the betray a lack of understanding by Metaverse was stillmore fantasy than reality. Best to look before you leap, distinguishing the tactically usable innovations from the pie-in-the-sky (often non-technical) people about futurism. what’s really going on.” Seismic shifts in the tech product universe only become a reality when the - TYLER GRIFFIN, RESTIV VENTURES innovation of tools is met with indisputable applications and user excitement. Be wary of anything deemed to be civilization-upending or offering 100x returns. Analyzing the Case for AI

WunderPredicts #7 Generative AI Explained Generative AI is best understood as an application of artificial intelligence that produces unique text and imagery based on human prompts. You might recall late 2022’s Lensa/DALL-E 2, Midjourney, andimage craze (everyone has a friend who got way too into AI profile photos). Show me the Money Venture Capital is bullish on AI alone -$2 billionfor AI-focused startups poured in in 2022 alone (an eye-watering sum in a year that ended on a historical low for funding). In 2022, Usage by Businesses Doubled 58 Avg. number of use cases is 3.8 in 2022, up from 1.9 in 50 56 50 2020 –however, benchmarks are skewed by high-tech 47 industries and use cases remain largely pie-in-the-sky for most brands’ tactical usage (e.g. –computer vision, robotic automation at scale, etc.) 20 AI Adoption 2017 2018 2019 2020 2021 2022

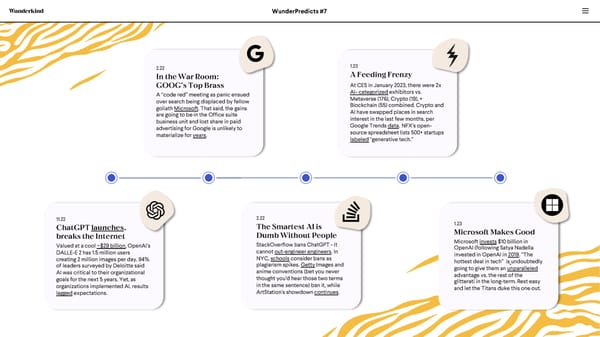

WunderPredicts #7 2.22 1.23 In the War Room: A Feeding Frenzy GOOG’s Top Brass At CES in January 2023, there were 2x A “code red” meeting as panic ensued AI-categorizedexhibitors vs. over search being displaced by fellow Metaverse (176),Crypto (19), + goliath Microsoft. That said, the gains Blockchain (55) combined. Crypto and are going to be in the Office suite AI have swapped places in search business unit and lost share in paid interest in the last few months, per advertising for Google is unlikely to Google Trends data. NFX’s open- materialize for years. source spreadsheet lists 500+ startups labeled“generative tech.” 11.22 2.22 ChatGPT launches, The Smartest AI is 1.23 breaks the Internet Dumb Without People Microsoft Makes Good Valued at a cool ~$29 billion, OpenAI’s StackOverflow bans ChatGPT -it Microsoft invests$10 billion in DALLE-E 2 has 1.5 million users cannot out-engineer engineers. In OpenAI (following Satya Nadella creating 2 million images per day. 94% NYC, schoolsconsider bans as invested in OpenAI in 2019. “The of leaders surveyed by Deloitte said plagiarism spikes. GettyImages and hottest deal in tech” is undoubtedly AI was critical to their organizational anime conventions (bet you never going to give them an unparalleled goals for the next 5 years. Yet, as thought you’d hear those two terms advantage vs. the rest of the organizations implemented AI, results in the same sentence) ban it, while glitterati in the long-term. Rest easy laggedexpectations. ArtStation’s showdown continues. and let the Titans duke this one out.

11:11 #7 d s Notes Done d Chat GPT – n n friend or foe? i e In a recession, more is more, and marketers often k need to work with less. In this case, we vote to r accept the friend request, but enter the relationship wisely. Leverage it to help with e m automation, content creation, thought-starters, market research, etc. -another support tool for d your arsenal. The Bottom Line -Generative AI's achievements, n om built on the backs of 2+ decades of machine learning research and development advances are c undoubtedly impressive —but the tech world's hype-bubble-to-bust cycle is swifter than ever, Wu Re too. Proceed with caution.

While businesses are slated to double-down on digital and tech investments, in tough times, few winners emerge. Fortune seems to favor the boldest, not the biggest. But where risk is hefty, rewards are super-sized. Grow Marketers must predicate spend strategy on growth-first channels, Better with rather than investing ever-more dollars into traditional paid channels that are expensive, unreliable, and fail to drive commensurate growth. Wunderkind Enter Wunderkind. o Wunderkind builds products for marketers who are goaled on generating revenue. o Wunderkind provides one-to-one customer experiences at unprecedented scale through channels that you own. o With the uncertainty surrounding the current economic environment, we offer performance guarantees that no other market solution can match.

Wunderkind is the performance marketing engine, powered by people–and we’ve championed privacy, creativity, and the power of the individual before it was cool. Here’s how we can partner to make 2023 the best one yet. Make the most of your Drive better performance and Invest in non-intrusive Website experience returns with Text + Email Ads that perform With the unparalleled scale of our Owned channels are the center of gravity of your WunderKIND Ads personifies its name – Identity Network, Wunderkind can help brand –now more than ever. Marketers have uniquely benefitting advertisers, publishers, you power your List Growth strategy doubled down on the efficiency of websites, andusers, by being rooted in a respect for that deliver more opt-ins than other email, text messaging, and mobile apps to make user experience. We offer the only high- leading solutions. This allows you to up for lost revenue and keep consumers engaged. impact, post-content ads in the market -i.e., target previously unavailable mid-funnel Not only do these Wunderkind channels drive our ads appear to users when they are prospects and drive net-new revenue revenue with efficiency and at scale, they’re also finished engaging with publisher content; from your email + text programs. far more secure than the traditional social media the most receptive juncture in their journey. platforms, placing the ownership of your customer Oh, and our performance metrics outpace data in your hands. industry benchmarks handily.